By Jacob Feist

Part 1 The Arguments For and Against Microcredits

In Poor Economics by Banerjee and Duflo, the authors outline the financial landscape in Africa. Their focus is on the concept of microfinancing and its potential benefit to developing nations. The key argument supporting microfinancing is that poor people in developing nations are constantly worrying and preparing for potential disaster. They rely on costly and potentially ineffective methods of savings. Thus, one can reasonably assume that there is a demand market for some sort of regulated borrowing and savings method.

Rutherford of the company SaveSafe explains that many families currently rely on savings clubs or self-help groups that allow multiple families to pool resources. Essentially, they are creating their own insurance float, proving that the concept is possible in developing nations. Additionally, many argue that as savings systems and financing systems become available, poor people would be able to create their own small businesses. Cases outlined by BRAC reveal that initial financing and basic guidance and education allows most people to create a revenue generator.

However, Banerjee and Duflo analyzed data sets of small businesses without BRAC guidance and concluded that the average small business in developing nations creates negative cash flow. Thus, leaving the business owner in the same positions as they were before the loan. This is compounded by the time and energy required to own and operate a small business. Additionally, the issues with microfinancing stem beyond the flaws in small businesses. Primarily, it is costly and risky managing small pools of wealth in developing nations. For a business, the cost of management will likely exceed the return on holdings. In countries, without systems of accountability, there is a risk that no one will repay their loans. Hence, to protect against risk banks would be forced to charge higher fees. These higher fees would create their own issues, as seen in the example of Jennifer Auma (Page 188). Her local bank’s withdraw fees negated any benefit of storing money.

Part 2 & 3 Microcredits in Tanzania

Microcredits were introduced in Tanzania in the 1990s and have been slowly integrated into society. Today, there are several banks offering microfinancing loans and savings for poor people in Tanzania. In 2001, these banks joined together under TAMFI, Tanzania Association of Microfinance Institutions. Together they work to develop the institutions themselves, government assistance, and microcredit availability. Moreover, the institution has proven successful, helping fund 1.2 million people with loans and savings.

Yet, there is still concern about the long-term success of these institutions. The World Bank analyzed the microfinancing landscape of Tanzania in 2003 and found some troubling results. In talking with government and bank officials, they found no discernable strategy for further developing their relationship or expanding the services of these banks. The World Bank was also displeased with regulatory bodies ability to promote transparency and accountability within these systems. Their biggest concern is human capacity. As the demand for microcredit institution increases as does the need for skilled labor in the banking sector. At this time, Tanzania is lacking skilled laborers to work in the microfinance and microcredit industry.

Part 4 Reflecting on “The Road to Ending Poverty”

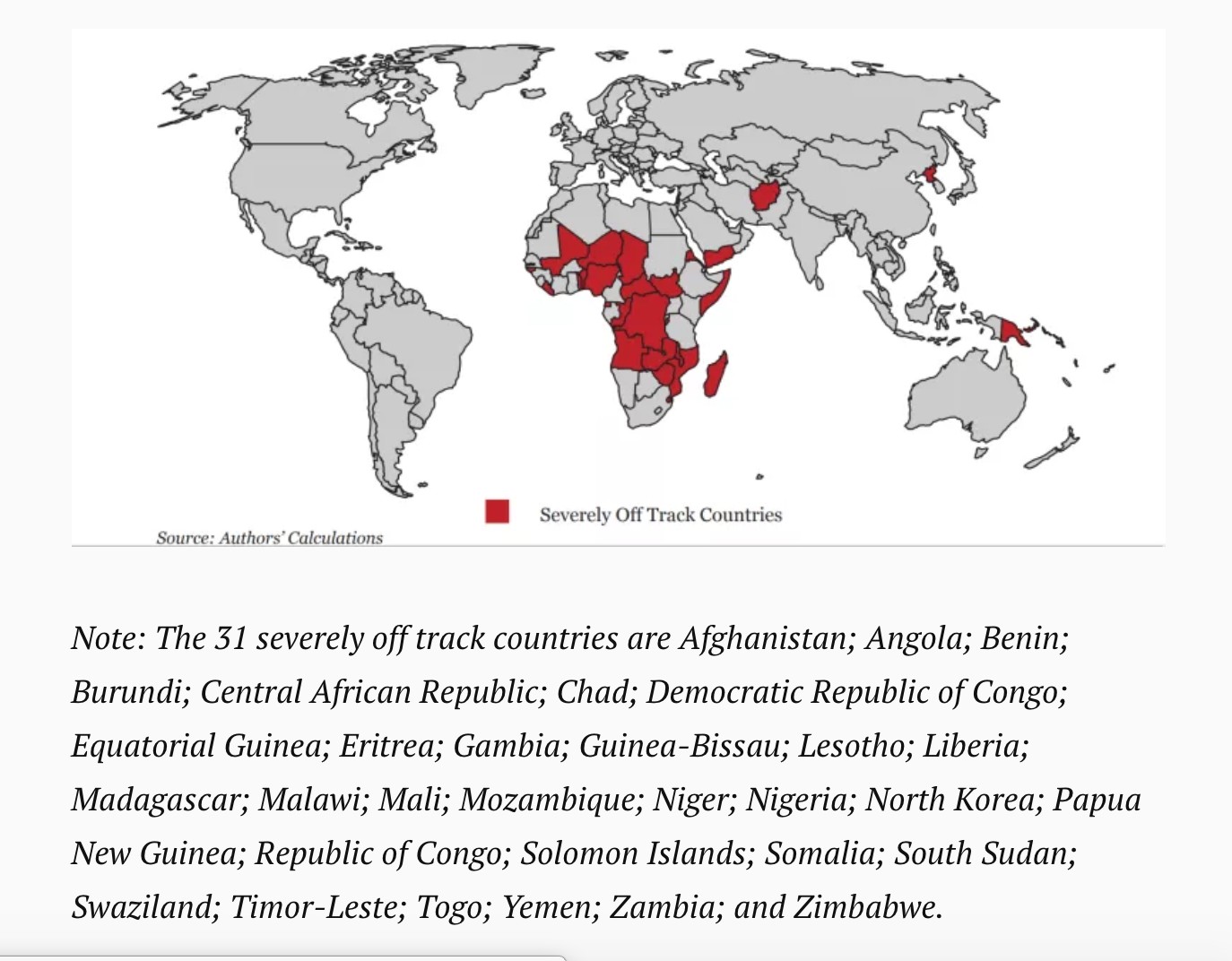

In the article “The road to ending poverty runs through 31 severely off track countries”, Gertz and Kharas outline a key issue in the fight against poverty. Many of the numbers contributing to the staggering drop in poverty is occurring within a few key nations. Countries like China and India have had huge economic booms leading to greater GDP and less poverty. The article cites that “7 of 10 countries cut their poverty headcount ratios by 70%.” While these are incredible results that will benefit large portions of humankind, they are misleading in outlining the overall success of the SDGs.

The countries experiencing the greatest success in eradicating poverty are typically those experiencing the greatest economic success. While this may appear obvious, it creates a dubious future for the remaining countries experiencing critical levels of poverty. The authors highlight 31 countries severely off track from meeting their goals. These countries range from radically unstable and underfunded to completely stagnant and receiving generous donations. Thus, the solution extends past simply promoting democracy or outside funding.

https://www.brookings.edu/blog/future-development/2018/02/13/the-road-to-ending-poverty-runs-through-31-severely-off-track-countries/

It also presents a glaring need for the SDGs and non-profit thinktanks across the world. Clearly, there is a need to adapt. Strategies must be developed for each of the remaining SOTC. While general SDGs and development projects have assisted many communities, it is clear that these cases follow no trend and require individual help. Hence, I feel that a summit similar to the original MDG meeting would be beneficial. There should be tasks and goals related to each nation, addressing critical needs, funding deficits, and areas of change. Moreover, in nations that funding is proving ineffective, reallocating recourses could prove effective.

Part 5 Technology as an Agent of Change

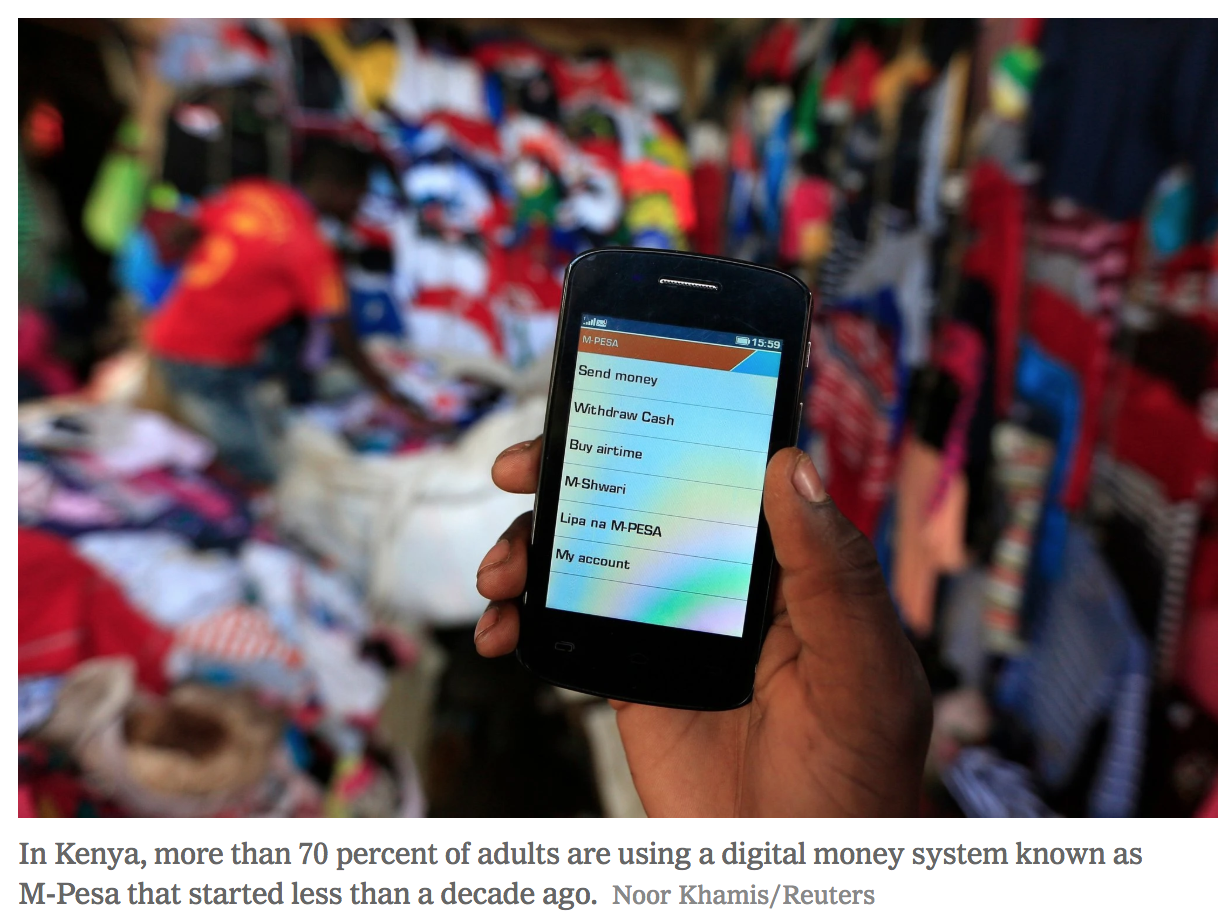

Technology is radically changing the way people spend and save money. McKinsey Consulting attributed a 6% rise in global spending to technology. Primarily, they are seeing enormous changes stemming from cell-phone use in developing nations. A New York Times article explains, “70% of adults are using [M-Pesa] that started less than a decade ago.” These microlending and financing institutions have created a spike in the transferring of funds and creation of small businesses.

https://www.nytimes.com/2016/09/22/business/dealbook/cellphones-not-banks-may-be-key-to-finance-in-the-developing-world.html?rref=collection%2Ftimestopic%2FMicrofinance&action=click&contentCollection=timestopics®ion=stream&module=stream_unit&version=latest&contentPlacement=3&pgtype=collection

Additionally, a 2017 World Bank Symposium outlined the success of microfinancing. The group of 35 tech and finance experts worked to explain the impact of technology and microcredits. They discovered six key elements impacted by the changes:

- Customer Centricity

- Reducing operational risks

- New business models

- Partnerships and collaboration

- Building trust

- Customer protection

Part 6 Reflecting on “Africa Poor Stealing Wealth”

The article outlines an important element preventing the distribution of wealth in Africa. Much of the wealth and recourses being developing in the continent is being exported or stolen. The facts detailed by Dearden present undeniable proof that industry is available. $203 Billion dollars left the country last year, including $68 billion dollars in avoided taxes. Additionally, $29 billion is lost annually to illegal wildlife and logging activity. This is exacerbated by the countries ultra-wealthy holding money in international tax havens.

Thus, it is clear that a solution must be developed. The author argues for repatriations and redistributions of wealth. However, I cannot fully support these solutions. Radical solutions often create radical problems. Attempting to take and redistribute the wealth of the ultra-wealthy will cause them to leave or store more money off-shore. Moreover, attempting to reduce tax havens is a noble cause, but one that would not be achievable without the backing of the entire international community. I believe the solution should start simple and then build outward. First, attack the explicitly illegal activities. Use funding to prevent illegal wildlife activity and outright tax evasion. Closing these cash flows could create an increase of almost $100 billion dollars.

Sources:

https://www.aljazeera.com/indepth/opinion/2017/05/africa-poor-stealing-wealth-170524063731884.html